News & Events

How a mutually-beneficial relationship between credit unions and auto dealerships fuels vehicle leasing in today’s affordability crisis

At CULA, our mission is to help credit unions offer vehicle leasing to their members, an auto finance option that is increasingly important as the average cost of a new vehicle skyrockets to $50,326. Our valued partners in this are credit unions, the foundation of our business. But, there is another set of partners who represent the secret sauce of credit union vehicle leasing: auto dealers. And that is reflected in the increase in the number of CULA’s dealer partners which, we are proud to say, grew 38% year over year in 2025 to hit its highest number ever.

So, what does this increase tell us about the synergy between auto dealers and credit unions? Well, for one, the intrinsic value of being able to offer a more affordable leasing option as car shoppers struggle with today’s skyrocketing payments and overall economic uncertainty. Affordability pressures are reshaping buyer behavior, driving the number of auto shoppers considering leasing, versus buying, to an all-time high[1]. Vehicle leasing is also a critical option for those hard-to-capture Gen Z car shoppers who are showing a distinct bias towards vehicle leasing[2]. For both auto dealers and credit unions, leasing is a golden opportunity to capture these customers early – and to keep them loyal for the long term.

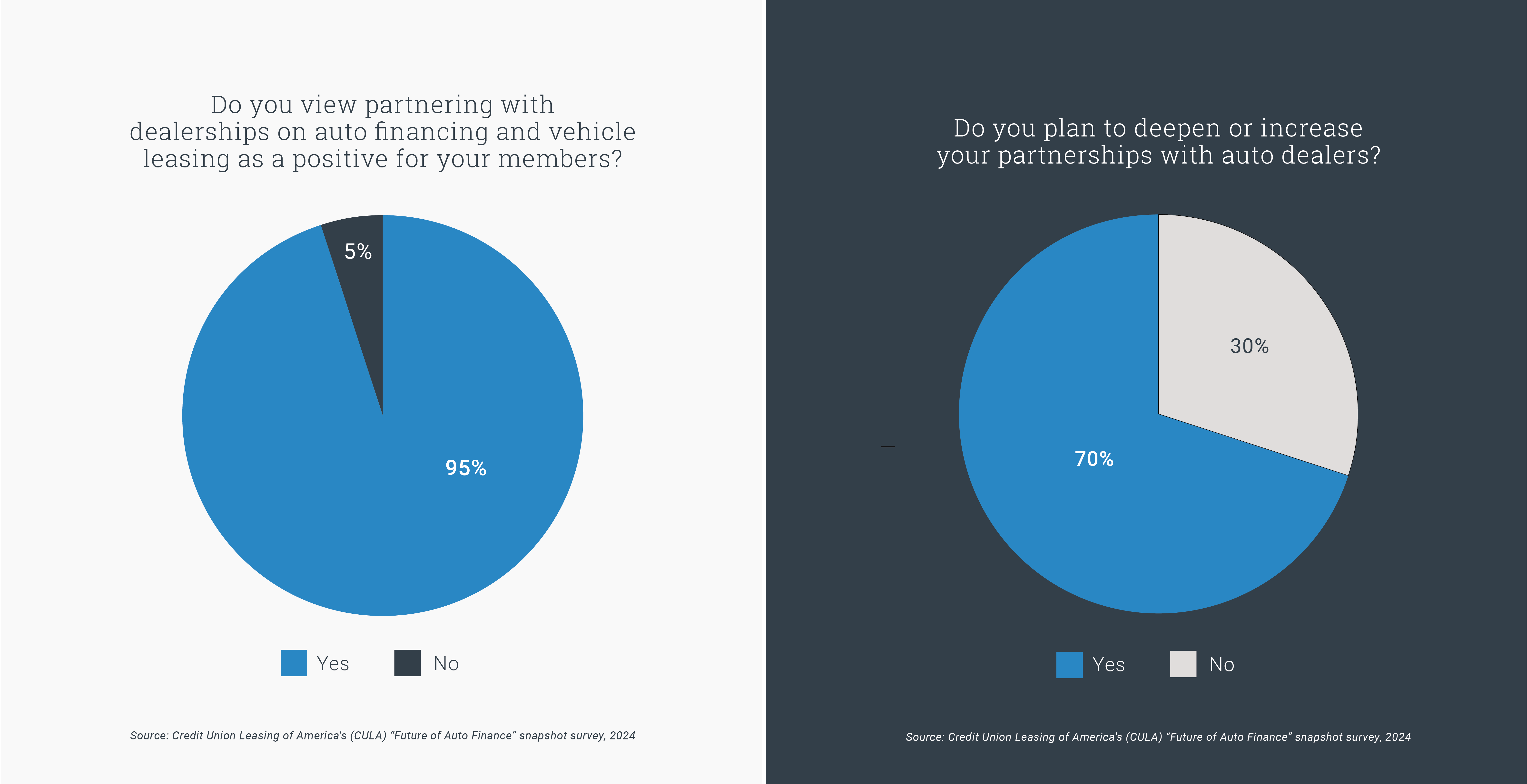

Our dealer partner growth numbers also underscore the deep value to credit unions of their dealer partnerships. But don’t just take our word for it: in a survey we conducted among credit union professionals, they were almost unanimous on the benefits of their partnerships with auto dealers, with 95% saying that partnering with dealerships on auto financing and vehicle leasing is a positive for their members. That same survey showed that 70% planned to deepen these partnerships – and, as our most recent numbers show, they clearly have.

Credit Unions and Dealerships: Leasing’s Mutual Beneficiaries

So, what is it that makes the dealer/credit union partnership such a win/win when it comes to leasing?

Here are just a few clues:

Credit Union Benefits:

● Localization – Partnering with dealers can help credit unions better understand local market demands, so they can develop tailored, affordable financing packages that align with consumer needs.

● Streamlined Approval Processes – Closer partnerships with dealers can enhance the streamlining of the financing approval processes, while providing quicker access and reducing time-related costs and complexities.

● Balancing Risk and Profitability – By leveraging insights they can only get from auto dealers, credit unions can identify viable lending opportunities that mitigate over-extension risks while ensuring reasonable returns.

● Long-Term Customer Relationships – Offering financing in concert with dealer partners helps credit unions build stronger, long-term relationships with members, fosters member loyalty and strengthens the credit union’s reputation in the community.

Auto Dealer Benefits:

● Affordability – Being able to offer customers the lowest monthly payments (vs auto loans) on many makes and models, benefits the customer and helps the dealer move the vehicle

● Flexibility – The option of greater term flexibility, (i.e. 36-month lease vs 84-month financing) at a similar payment, can increase an unsure customer’s likelihood to close.

● Insurance – Insurance is turnkey with Gap and $1000 wear and tear coverage included

● Remarketing – As used vehicle inventory increases, having used vehicle leasing options can help move more vehicles.

● Inventory – With some vehicle inventory continuing to be constrained, the ability to purchase the vehicle at lease-end is a significant value.

With few alternatives for dealers to their own captives, credit unions can help auto dealers find more flexible finance and mileage terms, as well as more products like used and new vehicle leasing, often with higher residual values, lower money factors, and larger reserve payouts. And, because CULA’s credit union leasing program is easy to use, this combination provides dealers with an alternative to the captive financing that is both efficient, practical, and lucrative.

In conclusion, the symbiosis between auto dealers and credit unions has never been more important than in today’s climate of uncertainty, disruption and economic challenges. In a world where AI seeks to create benefits by streamlining the human element out of the equation, the real-world relationship between auto dealers and credit unions is proven to generate efficiencies and tangible benefits for each part of the vehicle leasing equation – dealer, credit union and consumer. And, in today’s automotive landscape, that’s a win-win-win.

[1] According to the latest Cox Automotive Car Buyer Journey Study (January 2026)

[2] CU Times, January 2026: https://www.cutimes.com/2026/01/20/credit-unions-gateway-to-the-future-aligning-financial-products-with-gen-z-values/